Lafayette (765) 588-5080 | Indianapolis (317) 634-5968

Brownsburg (317) 836-5950

Informing You of Bankruptcy Alternatives in Indianapolis

While we absolutely have the means to assist you in filing a bankruptcy case, our firm also offers information regarding choosing bankruptcy alternatives. Please peruse the information below, and contact us with questions! We look forward to consulting with you and helping you lead a life free of financial stress.

Paying Debts with Retirement Savings

If you are struggling to pay your debts, or you’ve lost your income, you might be tempted to dip into your 401k plan or other retirement savings plan to cover expenses or pay creditors. All we can say is, please don’t do it!

Unfortunately, by the time most people in financial stress see an Indianapolis bankruptcy attorney, they’ve already gone through much if not all of their retirement savings trying to make ends meet and trying to avoid defaulting on debts and bankruptcy. The temptation to do this is certainly understandable. You don’t want to go back on your agreement to pay the debts. You want to maintain your good credit, and you might see bankruptcy as the last resort. But good financial planning involves looking at all the options and making a rational - not an emotional - decision about what is best for your family.

When you give up your retirement plan to pay a debt, you really are putting your long-term financial health at risk over a short-term problem of debt. Bankruptcy exemption laws allow us to protect your qualified retirement plan, including 401k, 403b, IRA, PERF, pension, and many other types of tax-deferred plans. So, if you file bankruptcy to eliminate your debts, you can keep these funds in your retirement plan and protect your ability to pay for your expenses when you reach retirement age.

Pulling money out of a retirement account can have massive tax consequences. Besides the immediate tax burden, pulling your money out costs much more in the long term by way of lost earnings. Here is an example:

Let’s assume you are 40 years old today and have $10,000 in your 401k. Even without contributing another penny to the plan, at typical performance rates, by age 65, you will have over $42,000 in the fund!

If instead of pulling money out, you eliminate your debts through bankruptcy, then you’ll have the available income to add money to your 401k plan going forward. Add just $1,000 per year to your 401k, and by age 65, you’ll have almost $98,000!

There are lots of misconceptions about the effects that bankruptcy will have on your financial health, credit, and other parts of your life that lead people to avoid bankruptcy at all cost. If you reside in the north central Indiana region and need a bankruptcy lawyer in Indianapolis, Brownsburg (or Greater Lafayette), please contact our bankruptcy attorneys.

Indianapolis Debt Consolidation

Debt consolidation involves getting a new loan to pay off your old creditors. This can reduce your monthly payments and make your debt more manageable, as long as you can afford the new payments. Some debt consolidation loans use your home equity as collateral for the loan.

Some of the downsides of debt consolidation include:

- High-interest rates - Because you already have lots of debt, you may only qualify for a high-interest rate consolidation loan. These loans can be very costly, even if the monthly payments are lower than the current situation.

- Temptation to incur more debt - If you just paid off all your credit cards using a consolidation loan, you suddenly have a large amount of available credit. The temptation can arise to start using the credit cards again, which now puts you in even more debt.

- Home as collateral - If you use a home equity line to obtain financing for your debt consolidation, your home becomes collateral for the debt. Debts that were previously unsecured and easily eliminated in bankruptcy, are now attached to your home, and likely will have to be paid if you want to keep the home.

- Loan Term - A debt consolidation loan will likely take anywhere from 5 to 30 years to repay. The harm to your credit from filing bankruptcy can be as little as 7 years, with potentially no requirement to repay any of the debt.

We offer consultations to discuss bankruptcy alternatives. If you reside in the north central Indiana region and need debt consolidation advice in Indianapolis (or greater Lafayette), please contact our bankruptcy attorneys.

Indianapolis Bankruptcy Alternatives: Debt Settlement

Debt Settlement involves contacting each of your creditors to attempt to negotiate a reduced balance. Creditors know that there is always a risk that they will get nothing, so they may be willing to accept partial payment to settle. However, in order to successfully settle large amounts of debt, you really need to have a lump sum of money available when you start.

Many creditors are willing to take as little as 40 or 50% of the amount they are owed if you are willing to pay it in a lump sum. However, if you have $30,000 of debt, you would need to have at least $15,000 in cash, available now, to have any hope of successfully settling for less than you owe.

Unfortunately, an industry of debt settlement companies has taken this concept and turned it into a very profitable business model that does little to help consumers. These companies tell you to stop paying your creditors and to pay them instead. They promise that if you pay them a certain amount for 3 or 4 years, they will save up your money and eventually settle with your creditors for 30-40% of what you owe. They usually sell you on the idea of avoiding bankruptcy and tell you that their system can minimize the damage to your credit. The truth is that anytime you stop paying at least your minimum payment, your credit will be damaged. Whether you are in a settlement program or preparing to file bankruptcy, or just not paying…the creditors will report your lack of payment just the same, and the harm will be exactly the same.

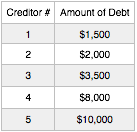

The main problem with debt settlement is that it simply takes too long to save up the required amount. Here is an example of a typical debt settlement situation. Let’s assume you owe $30,000 of total credit card debt to 5 different creditors as follows:

The debt settlement company might give you an estimate that this debt can be settled for $12,000-$15,000. If you have that much cash on hand, that might actually be true. (Though read ahead for some of the tax issues this causes, even if a settlement happens).

More realistically, you don’t have that kind of cash just laying around, so they suggest that you come up with the $15,000 by making 48 installments of $312.50. This sounds good because you’ve been paying $500 per month on your minimum credit card payments.

For the first few months, they will apply your entire payment to their fees, typically around $900 as a “retainer,” plus $75 or so per month as “maintenance fees.” (They also charge a settlement fee of about 15% of the settlement each time they settle an account, but to keep the math simple, we’ll ignore that fee for now). So, about four to five months after you start, you’ve only paid these initial fees. In month five or six, they start putting money into your “settlement account” with them, where the money to settle will start to build up.

After that, each month they are keeping $75 and putting about $237 into your settlement account. About four months later, they have enough saved up to contact Creditor #1 (that you owed $1,500) and offer to settle for half ($750). Let’s assume Creditor #1 is happy to settle. You see some progress because they notify you that they’ve eliminated your debt to Creditor #1. Great! Now, start over. Now you’ll start saving for Creditor #2. You’ll need about $1,000 to settle with them, so that will take about 4-5 months to save up. Creditor #2 is also willing to accept the $1,000 and they are eliminated.

We are now in month 15 of the plan. It has been over one year since Creditors #3, 4, and 5 have gotten any payment at all. They’ve been contacting you, but so far haven’t taken any real action. Eventually, they get tired of waiting, and Creditor #5 initiates a lawsuit. Within 3 months, that lawsuit has turned into a wage garnishment, and Creditor #5 is taking 25% of your wages…making it impossible to make any payments to the settlement company. Your settlement plan fails, and you are facing creditors 3, 4, and 5. They’ve been adding interest to your accounts over the last 18 months, so your balances to them now total over $30,000.

A year and a half after you started, you have negative credit reporting from all five creditors, more debt than you started with, and have lost over $5,600 in monthly payments that you can’t get back. Government agencies have been trying to go after some of these less-than-reputable companies with varying degrees of success. Attorneys General in several states have started to bring consumer protection lawsuits against the larger companies, but they simply don’t have the laws or manpower to keep up with the volume of companies out there.

One other issue: Remember how Creditor #1 and #2 accepted less than they were owed? You had a total of $1,750 of your debt to them “forgiven.” Those two creditors will be sending you a tax Form 1099 at the end of the year, and the IRS will likely be expecting you to pay income taxes on those $1,750 because cancellation of debt is considered a form of income.

All in all, debt settlement rarely works when done over time. Individual debts do have the potential to be settled if you have a lump sum of cash available. But the idea that you can save this money over a course of several years, while not making your minimum payments at the same time, and not get sued…that is practically impossible.

The bankruptcy attorneys at Perez & Perez will review your specific debt situation and help you determine the best option for your particular circumstances. We may suggest settlement over bankruptcy in the right circumstances, such as if you have only one or two creditors and access to large sums of money that can be used to settle. In those situations, we will be happy to assist you in negotiating a settlement with your creditors after fully explaining your options and the risks.

If you reside in the north central Indiana region and need a bankruptcy attorney for debt settlement in Indianapolis (or greater Lafayette), please contact us.

Disclaimer

We are a debt relief agency helping people file for relief under the bankruptcy code. The information contained herein is not legal advice. Any information you submit to Perez & Perez via this website may not be protected by attorney-client privilege. An attorney responsible for the content of this Site is Juan A. Perez Jr., licensed in Indiana with offices at 333 N. Alabama St., Ste 350A, Indianapolis, IN 46204.

Mailing address: PO Box 1019, Brownsburg, IN 46112

Email: contact@perezlawindiana.com

Indianapolis, IN 46204

(317) 634-5968

OTHER OFFICE LOCATIONS

Perez & Perez Bankruptcy

133 N. 4th Street, Ste 409

Lafayette, IN 47901

(765) 588-5080

Perez & Perez Bankruptcy

7230 Arbuckle Commons, Ste 152

Brownsburg, IN 46112

(317) 836-5950

![]()

![]()

![]()

![]()